Angeline C (iCompareLoan.com)

Australia is a popular investment destination among Singaporeans. And several banks in Singapore offer property investors an option to borrow, whether in SGD or a foreign currency.

If you have plans to buy a property in Australia, is it better to get a loan from a bank in Singapore or in Australia?

Banks in Singapore offer Singapore based investors the convenience of dealing with banks here and also perhaps a greater peace of mind when dealing with a bank you are familiar with and knowing that the bank is subject to strict regulations set by MAS.

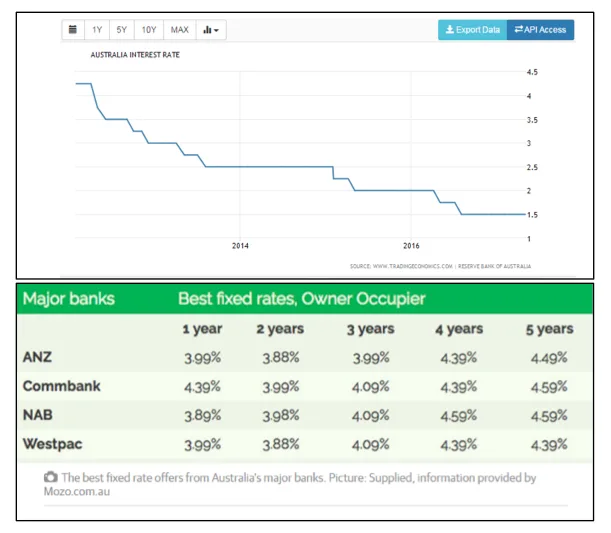

The interest rate offered are also typically lower. Loans offered by banks in Singapore are typically variable rate loans pegged to the SIBOR or board rate while lenders in Australia offer both fixed and variable rate loans (pegged to Reserve Bank of Australia rates). In recent months, the big four Australian banks, including Westpac and National Australia Bank were reported to have raised home loan interest rates for investor loans due to rising funding costs and greater regulation. In comparison, the rate from a lender in Singapore could be in the range of 3% +. This is despite the fact that Australian cash interest rates are at a 5 year low of 1.5%, Australian lenders typically charge 4+% to 5% for AUD property loans.

Figure 1: Australia Interest Rate, Australian Property Loan rates by Major banks, Trading Economics, Reserve Bank of Australia, Mozo, Geelongadvertiser, iCompareLoan.com

In Singapore, borrowers have the option of a SGD or AUD or multi-currency loan but taking a non-AUD loan would involve forex risk since the property is denominated in AUD. This could subject the borrower to a margin call when the AUD depreciates against the base currency.

Eg: In 2014, Mr Lim bought an Australian property at A$900,000 and took up a loan of the Singapore dollar equivalent of A$630,000 (70% LTV). Assuming the exchange rate at A$/S$ = 1.15, the loan translates to S$724,000.

Now, the outstanding loan is S$800,000. Assuming an exchange rate of A$/S$ = 1.03, the loan is A$776,699 which represents a LTV of 86% assuming the valuation stays at A$900,000. This would trigger a top up to rebalance the LTV to 70%.

Taking a loan from a Singapore lender means it would be subject to MAS regulations such as the total debt servicing ratio or TDSR.

The maximum age limit is lower at up to 75 years for Singapore lenders vs 99 years in Australia.

The loan to valuation (LTV) will vary depending on whether you are an Australian citizen, permanent resident or non resident, self employed or hold temporary visa. It ranges from 70% at a Singapore lender to 80% at an Australian bank.