Cracking the Australian property market ain’t easy. Not only is it one of the world’s most expensive places to buy, but houses here always seem to sell way above their asking prices. In fact, data compiled over a recent six-month period by property app Homer reveals that in some parts of the country, properties are selling for more than $100,000 above the guide. That’s pretty wild, considering you could buy an entire house for that sum back in the 1980s.

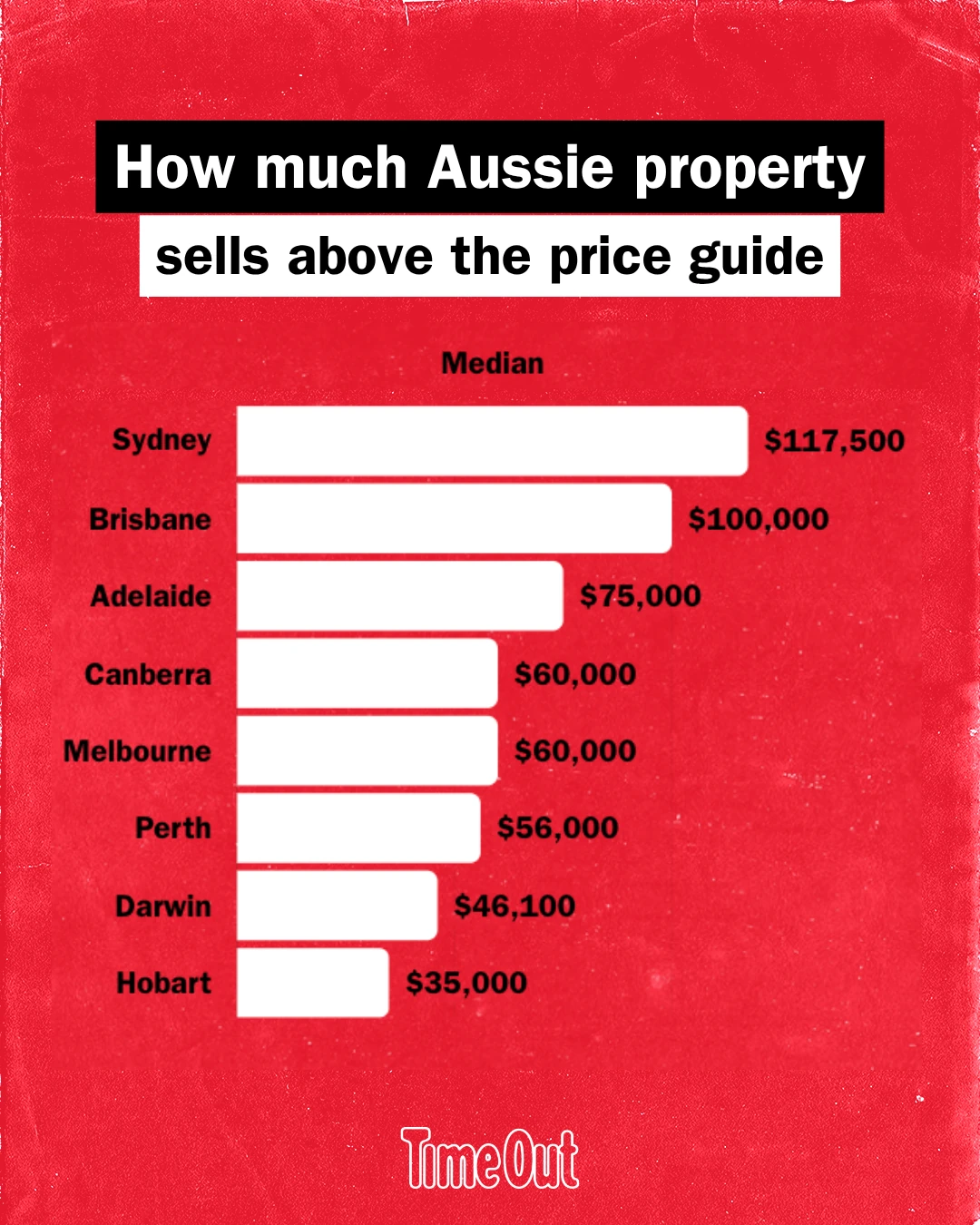

Perth leads the country’s property boom, with 76 per cent of sales exceeding the top of the price guide by a median of $56,000. Adelaide follows, with 73 per cent of properties smashing the asking price at an even higher median of $75,000.

Unsurprisingly, Sydney sale prices tend to overshoot the top of the price guide figure by the most in Australia, selling for a median of $117,500 above the advertised guide. Brisbane buyers are facing a similar reality, paying a median of $100,000 above expectations.

Interestingly, Melbourne is the only capital city where properties are more likely to sell below the price guide (53 per cent) than above (37 per cent). That difference becomes even more evident in regional Victoria, where a massive 71 per cent of properties sell below the advertised price.

While laws exist to prevent deliberate underquoting in NSW and Victoria – with agents risking fines of up to $110,000 – a house selling for more than its price guide doesn’t necessarily mean that the agent has broken the law, especially given how unpredictable auctions can be.

However, this may start to change following the Federal Government’s latest Budget tax reforms. Last week, more capital city homes failed at auction than sold, suggesting upcoming Cotality data will show the “clearance rate” (the rate of properties sold at auction) has been dragged below 50 per cent for the first time in six years. Good news for those looking to purchase property – not so much for those wanting to sell.